5 mins read

The Next Wave: How Gen Z Is Redefining Spending Culture vs Millennials

Gen Z vs Millennials: Spending Culture Comparison

Generation Z (born ~1997–2012) and Millennials (born ~1981–1996) are two powerhouse cohorts shaping how money flows and markets evolve. With unique mindsets rooted in their formative experiences, their spending cultures reveal both contrasts and future economic implications. Let’s dive deep into these differences and their larger economic impact.

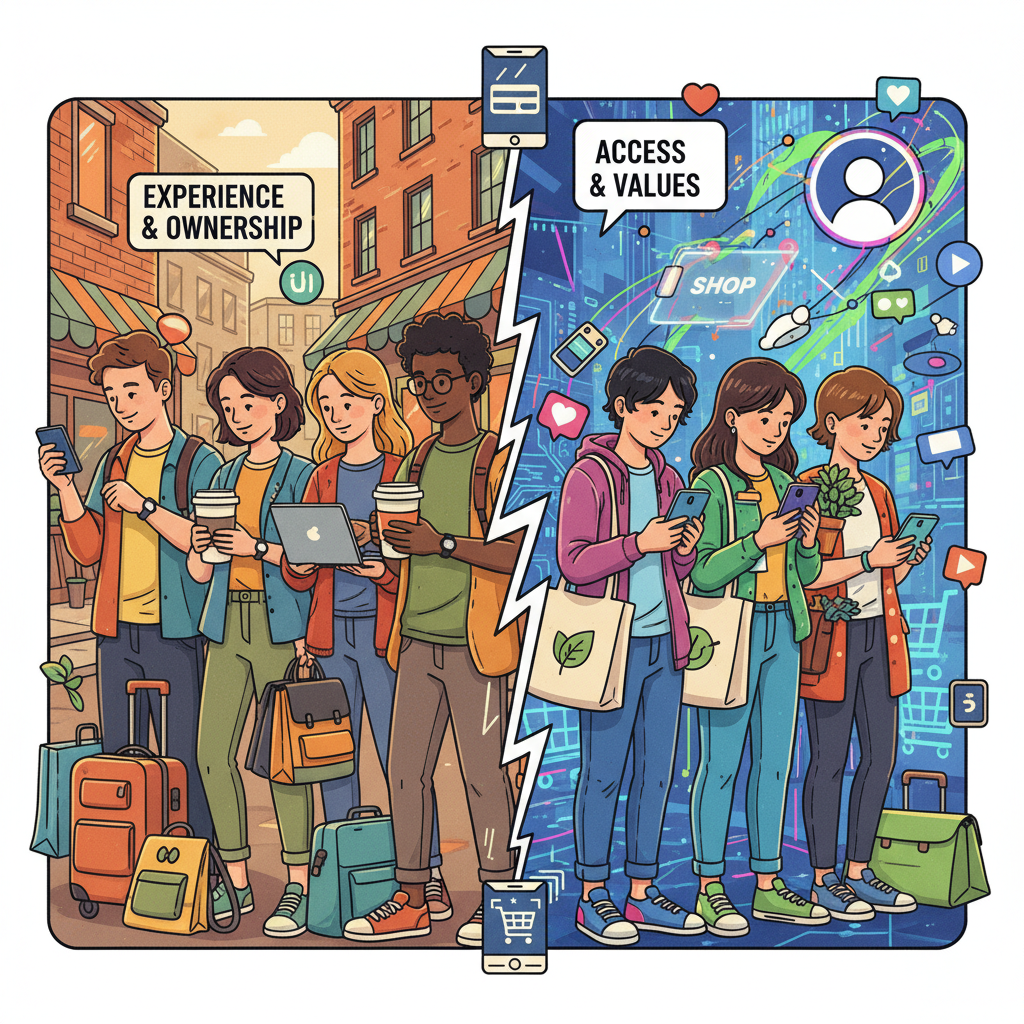

Millennials’ Spending Culture

- Experience-driven: Favor travel, dining, socializing, and wellness as investments in personal satisfaction.

- Omnichannel shoppers: Value researching online but often buy in-store, seeking best-of-both-worlds experiences.

- Higher absolute savings: Often have established careers and are more likely to maintain substantial emergency buffers.

- Brand loyalty: Relate to brands with proven reliability, eco-friendliness, and customer service.

- Traditional financial tools: Use credit cards primarily, avoiding high-interest debt when possible.

Gen Z’s Spending Culture

- Digital natives: Make purchases via mobile and social platforms, trusting authenticity and influencer recommendations.

- Affordability + ethics: Seek deals, value-conscious purchases, and support brands with strong social commitments.

- Impulse + social commerce: Frequently make small, impulsive purchases, often driven by social media.

- Relatively high savings rate: Save/invest early despite lower absolute balances due to gig economy work & economic uncertainty.

- Flexible payment choices: Heavy use of Buy Now Pay Later (BNPL), digital wallets, and alternative finance products.

Key Differences at a Glance

| Aspect | Millennials | Gen Z |

|---|---|---|

| Saving Habits | Higher total savings; focus on long-term buffers 25% have 6-month emergency funds |

Higher savings rate as % of income; thinner buffers Only 10% have 6-month funds |

| Spending Priorities | Enriching experiences, quality products | Affordability, trend-driven, inclusive and ethical brands |

| Shopping Channels | Hybrid: online research + in-store buys | Mobile-first social commerce, fast app adoption |

| Purchase Influences | Peer reviews, traditional ads, brand trust | Influencers, viral content, social trends |

| Brand Loyalty | Consistent, value-based relationships | Low loyalty, quick to switch for deals or new features |

| Debt & Payment | Credit cards, long-term finance | BNPL, digital wallets, short-term, flexible options |

| Sustainability Focus | Eco-friendliness, corporate responsibility | Ethics + affordability, demand transparency and inclusivity |

Detailed Explanations

- Saving Habits: Millennials’ higher savings buffers stem from life-stage advantages, job stability, and post-2008 caution. Gen Z is more proactive on a personal finance level but tends to have thinner cash reserves due to gig work and student debt.

- Spending Priorities: Millennials splurge on lasting memories. Gen Z prefers instantly gratifying, small purchases, often focused on self-expression and affordability.

- Shopping Channels: Millennials bridge online and brick-and-mortar, while Gen Z seamlessly shops on mobile and social platforms, expecting frictionless experiences.

- Purchase Influences: Social media is king for Gen Z—more than 80% of their purchases are influenced by what’s trending or recommended by influencers, while Millennials still weigh user reviews and brand trust heavily.

- Brand Loyalty: Millennials stick with brands that align with their values; Gen Z shifts quickly based on trends, price, or features.

- Debt & Payment: Credit cards are the norm for Millennials; Gen Z opts for modern options like BNPL and digital wallets to manage cash flow.

- Sustainability Focus: Both care, but Gen Z places higher demands on brands for ethics, inclusivity, and transparency, and will abandon brands that don’t align.

Conclusion & Future Economic Impact

The growing influence of Gen Z is set to reshape spending dynamics and the economy in several pivotal ways:

- Rapid shifts in demand: As Gen Z’s disposable income rises, expect businesses to innovate quicker to keep up with viral trends and evolving preferences. Products and brands will need to be adaptive, affordable, and aligned with social causes to thrive.

- Explosion of social commerce & digital payments: With Gen Z at the helm, mobile shopping, influencer-driven purchases, and payment flexibility (BNPL, e-wallets) will dominate, potentially reshaping the retail and fintech industries.

- Pressure on brand accountability: Gen Z’s insistence on ethics, inclusivity, and sustainability will force brands and even policy-makers to increase transparency and adopt stronger ESG (Environmental, Social, Governance) practices.

- Economic volatility & resilience: While flexible spending and lighter brand loyalty can drive innovation, they may also intensify demand unpredictability. This rapid change could impact traditional players and accelerate cycles of boom-bust in certain sectors.

- Investment and saving trends: Gen Z’s early entry into investing, despite lower incomes, may boost retail investor participation, democratize finance, and push for more accessible wealth-building tools.

In summary: Gen Z’s spending will amplify digital transformation, challenge businesses to be agile and trustworthy, and drive a more values-conscious economy. The next decade will see brands and economies pivot to serve this confident, tech-savvy, and uncompromising generation—potentially making commerce both more dynamic and inclusive.